Last updated: February 26, 2026

When Sarah opened her credit report and saw a $3,200 charge-off from a credit card she’d fallen behind on during a medical emergency, her first instinct was to search for help. She found dozens of credit repair companies promising to “erase” charge-offs and “boost her score 100 points in 30 days.” But can credit repair companies remove charge offs, or are these promises too good to be true?

The short answer: Credit repair companies can legally dispute charge-offs under the Fair Credit Reporting Act (FCRA), but they cannot legally remove accurate, legitimate charge-offs from your credit report[1][6]. What they can do is challenge inaccuracies, help negotiate pay-for-delete agreements, and guide you through the dispute process—but any company guaranteeing removal of accurate negative information is violating federal law.

Key Takeaways

- Credit repair companies can dispute charge-offs but cannot legally delete accurate, current information from your credit report

- The Credit Repair Organizations Act (CROA) prohibits companies from guaranteeing removal of legitimate negative items[3]

- Charge-offs automatically fall off credit reports seven years from the original delinquency date, regardless of payment status[1][2]

- Inaccurate charge-off details (wrong amounts, dates, or creditor names) can be successfully disputed and removed[1][2]

- Pay-for-delete negotiations offer the most realistic path to removing legitimate charge-offs, though creditors aren’t legally required to comply[2]

- The FTC warns consumers that no one can legally remove accurate information, making promises of guaranteed removal a red flag[6]

- Dispute investigations take 30-45 days by law, so companies promising rapid removal in days are using misleading tactics[1]

- DIY credit repair is free and follows the same legal process as paid services, making it a viable alternative for many consumers

Quick Answer

Credit repair companies can dispute charge-offs on your behalf, but they cannot legally remove accurate, verifiable charge-offs from your credit report. Under the FCRA, they can challenge reporting errors and negotiate with creditors, but the Credit Repair Organizations Act prohibits guaranteeing removal of legitimate negative information[3][6]. Your best options are disputing genuine inaccuracies, negotiating pay-for-delete agreements, or waiting for the automatic seven-year removal timeline.

What Is a Charge-Off and How Does It Affect Your Credit?

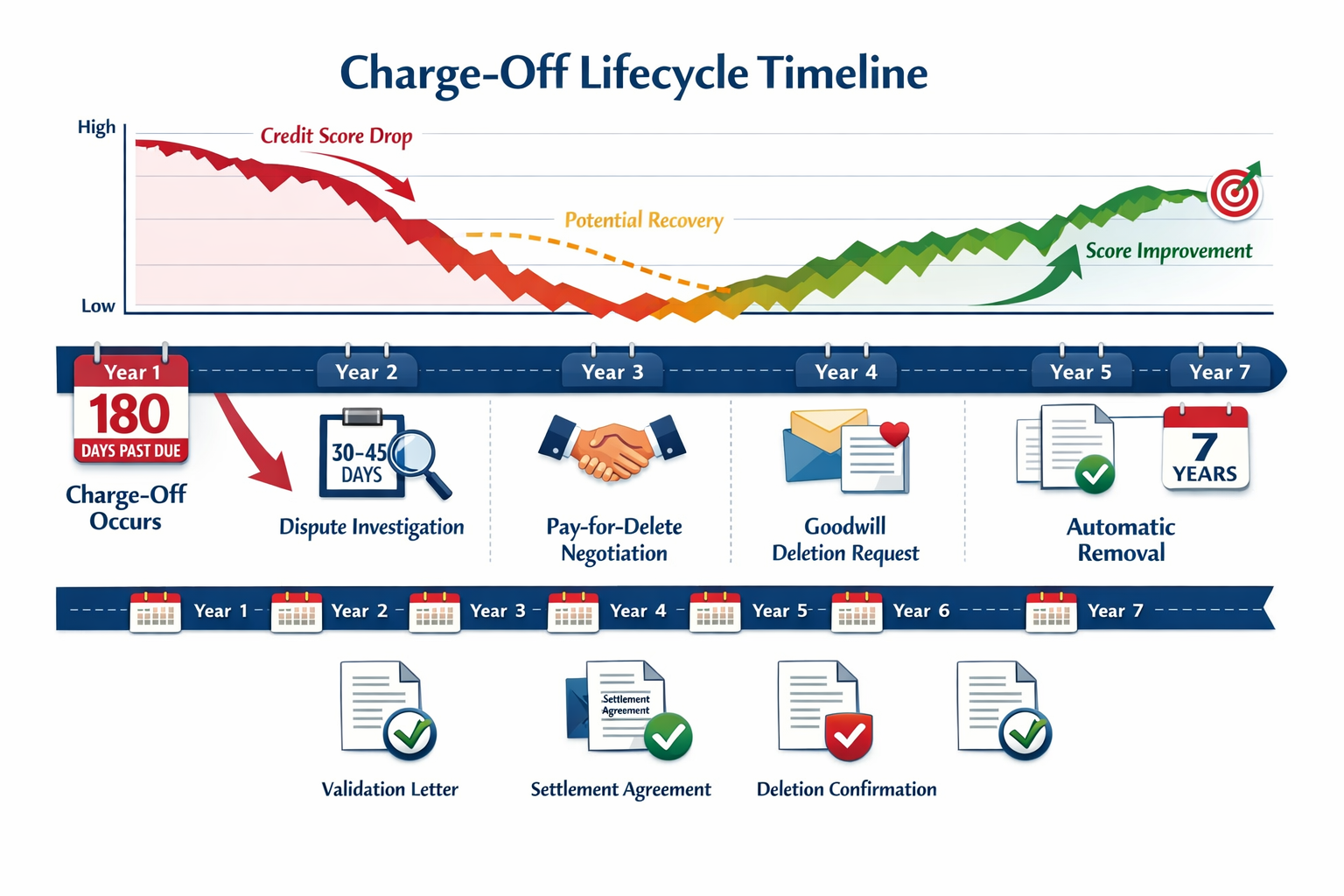

A charge-off occurs when a creditor writes off your debt as a loss after you’ve failed to make payments for approximately 180 days (six months). The creditor essentially gives up on collecting the full amount and reports the account as “charged off” to the credit bureaus.

Here’s what happens when an account gets charged off:

- Your credit score typically drops 60-110 points, depending on your starting score and credit history

- The charge-off remains on your credit report for seven years from the original delinquency date[1][2]

- You still legally owe the debt—charging off doesn’t erase what you owe

- The creditor may sell your debt to a collection agency, which can then pursue payment

- Future lenders see you as a higher-risk borrower, making loan approvals harder and interest rates higher

Common mistake: Many people think paying off a charge-off removes it from their credit report. In reality, the status simply updates to “paid charge-off,” which still negatively impacts your credit, though less severely than an unpaid charge-off.

The charge-off stays visible to lenders for the full seven-year period whether you pay it or not, though paying it can improve your chances of mortgage or auto loan approval.

Can Credit Repair Companies Remove Charge-Offs Legally?

Yes, credit repair companies can legally work to remove charge-offs, but only under specific circumstances and within strict legal boundaries. They cannot remove accurate, verifiable information—doing so would violate federal law[6].

What credit repair companies can legally do:

- Dispute inaccurate information: If the charge-off contains errors (wrong balance, incorrect dates, creditor name mistakes), they can file disputes with credit bureaus[1][2]

- Request debt validation: They can demand that creditors prove the debt is legitimate and accurately reported under the Fair Debt Collection Practices Act (FDCPA)[1]

- Negotiate pay-for-delete agreements: They can contact creditors on your behalf to negotiate removal in exchange for payment, though creditors aren’t required to agree[1][2]

- Submit goodwill deletion requests: For customers with otherwise strong payment histories, they can ask creditors to remove the charge-off as a courtesy[1]

What they cannot legally do:

- Guarantee removal of accurate charge-offs (violates CROA)[3]

- Create false disputes or misrepresent information

- Remove accurate information that’s less than seven years old[6]

- Promise specific credit score increases or removal timelines

The Federal Trade Commission explicitly warns that “no one can legally remove accurate and timely negative information from a credit report”[6]. Companies that promise otherwise are either misleading you or planning to use illegal tactics that could expose you to legal risk.

Choose a credit repair company if: You’ve identified errors but find the dispute process overwhelming, you’re negotiating with multiple creditors, or you lack time to manage disputes yourself. Choose DIY repair if the errors are straightforward and you’re comfortable writing letters and following up.

How Do Credit Repair Companies Actually Remove Charge-Offs?

Credit repair companies use several legitimate strategies to challenge charge-offs, though success depends entirely on whether the charge-off contains errors or if the creditor agrees to negotiate.

The Dispute Process for Inaccurate Information

Credit repair companies follow a structured process when they find reporting errors:

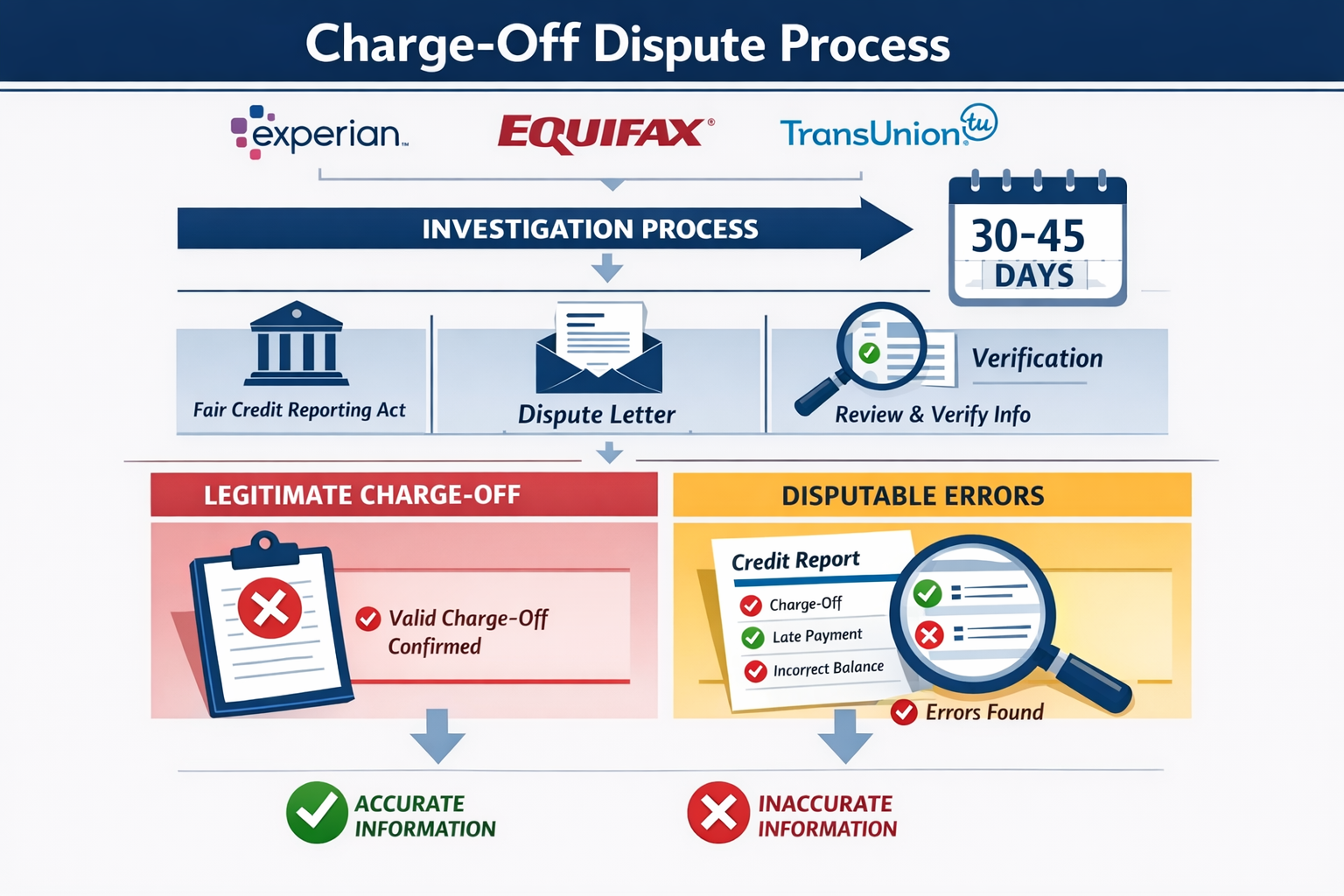

- Credit report analysis: They review reports from all three bureaus (Experian, Equifax, TransUnion) to identify inaccuracies in the charge-off listing

- Dispute letter submission: They send formal dispute letters to credit bureaus citing specific errors (wrong dates, amounts, account numbers, or creditor details)[1][2]

- Bureau investigation: Credit bureaus have 30-45 days to investigate by contacting the creditor to verify the information[1]

- Creditor response: If the creditor cannot verify the disputed information or doesn’t respond within the timeframe, the bureau must remove the charge-off

- Follow-up: If the dispute is rejected, they may submit additional evidence or escalate the dispute

Common errors that can lead to successful removal:

- Incorrect charge-off date or amount

- Wrong account number or creditor name

- Duplicate charge-offs (same debt reported multiple times)

- Charge-offs older than seven years from the original delinquency date

- Accounts that were never yours (identity theft or mixed files)

Pay-for-Delete Negotiations

The most realistic strategy for removing legitimate charge-offs involves negotiating directly with creditors or collection agencies:

How pay-for-delete works:

- The credit repair company contacts the creditor offering to settle the debt (often for less than the full amount)

- In exchange for payment, they request written agreement that the creditor will delete the charge-off from all credit reports

- Once payment is made and clears, the creditor should contact the bureaus to remove the entry

Important limitation: Creditors have no legal obligation to agree to pay-for-delete, and many major creditors have policies against it[2]. Original creditors are often less willing than collection agencies to negotiate deletion.

Edge case: Some creditors will agree to pay-for-delete verbally but won’t provide written confirmation. Without written proof, you have no recourse if they fail to delete the charge-off after you pay. Always insist on written agreements before making payment.

Goodwill Deletion Requests

For customers who had a strong payment history before the charge-off and can explain extenuating circumstances (medical emergency, job loss, natural disaster), credit repair companies may submit goodwill letters asking creditors to remove the charge-off as a courtesy[1].

These requests work best when:

- You’ve since paid the debt in full

- You have a long history with the creditor

- The charge-off was an isolated incident

- You can document the hardship that caused the missed payments

Success rates for goodwill deletions are low, but they cost nothing to attempt and occasionally work with smaller creditors or credit unions.

What Success Rate Can You Expect from Credit Repair Companies?

Credit repair companies often advertise success rates of 70-80%, but these numbers are misleading because they typically reflect all disputes, not specifically charge-off removals[1].

Realistic expectations for charge-off removal:

| Scenario | Estimated Success Rate | Timeline |

|---|---|---|

| Charge-off with clear reporting errors | 60-80% | 30-90 days |

| Legitimate charge-off with pay-for-delete negotiation | 20-40% | 60-180 days |

| Goodwill deletion request | 5-15% | 30-60 days |

| Accurate charge-off with no errors or negotiation | Near 0% | N/A |

The harsh reality: If your charge-off is accurate and the creditor refuses to negotiate, no credit repair company can legally remove it. You’ll need to wait for the seven-year automatic removal period[1][2].

Red flags indicating unrealistic promises:

- Guarantees of specific point increases or removal timelines

- Claims they can remove any negative item regardless of accuracy

- Promises of results in days or weeks (disputes legally take 30-45 days)[1]

- Requests for payment before services are rendered (illegal under CROA)[3]

- Suggestions to create a new credit identity or dispute accurate information

When Marcus hired a credit repair company that promised to remove his three charge-offs “within 30 days guaranteed,” he paid $500 upfront. Three months later, all three charge-offs remained on his report because they were accurate. The company had simply filed frivolous disputes that were quickly verified and rejected. He lost his money and wasted time he could have spent negotiating pay-for-delete agreements himself.

Should You Hire a Credit Repair Company or Do It Yourself?

You can legally do everything a credit repair company does, and the process is identical whether you hire help or handle it yourself. The decision comes down to time, complexity, and confidence.

Advantages of DIY credit repair:

- Zero cost: Disputing errors and negotiating with creditors is free when you do it yourself

- Direct control: You manage timelines and communication directly

- Learning experience: Understanding credit repair helps you maintain good credit long-term

- No risk of scams: You avoid potentially fraudulent credit repair companies

Advantages of hiring a credit repair company:

- Time savings: They handle the paperwork, follow-ups, and creditor negotiations

- Experience with creditors: Established companies may have relationships that improve negotiation success

- Managing multiple disputes: If you have numerous errors across multiple accounts, professional help can streamline the process

- Legal knowledge: Reputable companies understand FCRA, FDCPA, and CROA requirements

Cost comparison:

- DIY: $0 (only postage for certified mail, typically $10-20 total)

- Credit repair companies: $50-150 per month, typically requiring 3-6 month commitments[4]

Choose DIY if: You have one or two charge-offs to address, the errors are straightforward, you’re comfortable writing formal letters, and you have time to track disputes.

Choose a credit repair company if: You have multiple complex errors across several accounts, you lack time for the administrative work, you’re uncomfortable negotiating, or you’ve tried DIY without success.

Common mistake: Hiring a credit repair company for accurate charge-offs with no errors. No company can legally remove accurate information, so you’d be paying for services that cannot deliver results[6].

How Long Does It Take to Remove a Charge-Off?

The timeline for charge-off removal varies dramatically based on the method used and whether the charge-off is accurate or contains errors.

Timeline by removal method:

Disputing inaccurate information:

- Initial dispute submission: 1-7 days

- Credit bureau investigation: 30-45 days (required by law)[1]

- Creditor response and bureau decision: 30-45 days

- Total timeline: 60-90 days for first dispute attempt

- Multiple dispute rounds (if initial dispute fails): 4-6 months

Pay-for-delete negotiation:

- Finding contact information and initiating negotiation: 1-2 weeks

- Back-and-forth negotiation: 2-8 weeks

- Payment processing: 1-2 weeks

- Creditor reporting deletion to bureaus: 30-60 days

- Total timeline: 2-4 months

Goodwill deletion request:

- Letter drafting and submission: 1 week

- Creditor review: 2-6 weeks

- Total timeline: 3-7 weeks (though most are denied)

Automatic removal:

- Seven years from the original delinquency date (not the charge-off date)[1][2]

- Happens automatically without any action required

Important timing detail: The seven-year clock starts from the date you first became delinquent before the charge-off, not the charge-off date itself. If you stopped paying in January 2020 and the account charged off in July 2020, the charge-off must be removed by January 2027.

Companies promising removal “within days” or “guaranteed in 30 days” are violating realistic timelines since credit bureaus legally have 30-45 days just to investigate disputes[1].

What Are the Alternatives to Credit Repair Companies?

Several alternatives exist for addressing charge-offs without hiring a credit repair service.

Negotiate Directly with Creditors

You can contact creditors yourself to negotiate pay-for-delete agreements or settlement offers:

Steps for direct negotiation:

- Request debt validation via certified mail to confirm the debt is legitimate

- Research typical settlement amounts (often 30-60% of the balance)

- Call the creditor’s collections department and ask to speak with someone authorized to negotiate

- Propose a settlement amount in exchange for deletion from credit reports

- Get the agreement in writing before making any payment

- Keep records of all communications and payment confirmations

Advantage: You save monthly credit repair fees and maintain direct control.

Disadvantage: Creditors may be less responsive to individual consumers than to established credit repair companies.

File Disputes Yourself

You can submit disputes directly to credit bureaus online, by mail, or by phone:

DIY dispute process:

- Obtain free credit reports from AnnualCreditReport.com

- Identify specific errors in the charge-off listing

- Write a dispute letter citing the errors and requesting investigation

- Send via certified mail with return receipt to each bureau reporting the error

- Wait 30-45 days for investigation results

- Follow up if the dispute is rejected with additional evidence

The Consumer Financial Protection Bureau provides free dispute letter templates on their website.

Work with Nonprofit Credit Counseling

Nonprofit credit counseling agencies accredited by the National Foundation for Credit Counseling (NFCC) offer free or low-cost guidance:

- Credit report review and error identification

- Budgeting assistance to prevent future charge-offs

- Debt management plans that may improve creditor relationships

- Education on credit building strategies

Unlike for-profit credit repair companies, nonprofit counselors don’t charge monthly fees and focus on long-term financial health rather than quick fixes.

Wait for Automatic Removal

If the charge-off is accurate and creditors won’t negotiate, your most reliable option is simply waiting for the seven-year automatic removal[1][2]. During this time:

- Focus on building positive credit with secured credit cards or credit-builder loans

- Make all current payments on time

- Keep credit utilization below 30%

- Avoid new negative items

A charge-off’s impact on your credit score diminishes over time, especially if you build positive payment history. After 3-4 years, the damage is significantly less severe than in the first year.

Common Mistakes When Trying to Remove Charge-Offs

Avoiding these errors can save you money and prevent making your credit situation worse:

Paying before getting written deletion agreements: Many consumers pay settled amounts only to find the charge-off remains on their report because they didn’t secure written confirmation of deletion[2].

Disputing accurate information repeatedly: Filing multiple frivolous disputes on accurate charge-offs can backfire. Creditors may add detailed notes to your credit file, and bureaus may label your disputes as frivolous, making future legitimate disputes harder[1].

Falling for “new credit identity” scams: Some disreputable companies suggest applying for an Employer Identification Number (EIN) to create a “new credit identity.” This is illegal and constitutes fraud.

Paying upfront fees: CROA prohibits credit repair companies from charging fees before completing services[3]. Companies requesting upfront payment are violating federal law.

Ignoring statute of limitations confusion: The seven-year credit reporting period is separate from your state’s statute of limitations for debt collection lawsuits. Paying an old debt can restart the lawsuit clock in some states, even though it doesn’t extend credit reporting.

Accepting verbal agreements: Always insist on written pay-for-delete agreements. Verbal promises are unenforceable and leave you with no recourse if the creditor doesn’t follow through.

Stopping payments on current accounts: Some consumers become so focused on old charge-offs that they neglect current accounts, creating new negative items that damage their credit further.

Frequently Asked Questions

Can credit repair companies guarantee charge-off removal?

No. The Credit Repair Organizations Act prohibits companies from guaranteeing removal of accurate negative information[3]. Any company making such guarantees is violating federal law and should be avoided.

How much do credit repair companies charge to remove charge-offs?

Most credit repair companies charge $50-150 per month with typical engagements lasting 3-6 months, totaling $300-900[4]. However, they cannot charge before completing services under CROA[3].

Will paying a charge-off remove it from my credit report?

No. Paying a charge-off updates the status to “paid charge-off” but doesn’t remove it from your report. It remains for seven years from the original delinquency date unless you negotiate a pay-for-delete agreement[2].

Can I remove a charge-off after 7 years?

Charge-offs must automatically be removed after seven years from the original delinquency date[1][2]. If one remains after this period, dispute it with the credit bureaus citing the FCRA’s seven-year requirement.

Do charge-offs hurt my credit if they’re paid?

Yes, though less than unpaid charge-offs. Paid charge-offs still indicate past serious delinquency to lenders. The impact decreases over time, especially with positive payment history on other accounts.

Can I negotiate a charge-off myself without a credit repair company?

Absolutely. You can contact creditors directly to negotiate pay-for-delete agreements or settlements. The process is identical whether you hire help or do it yourself, and DIY saves you monthly fees.

What’s the difference between a charge-off and a collection account?

A charge-off is the creditor writing off your debt as a loss. A collection account appears when the creditor sells your debt to a collection agency. Both can appear on your credit report simultaneously for the same debt.

Are there any legal ways to remove accurate charge-offs immediately?

No. Accurate charge-offs cannot be legally removed immediately. Your only options are negotiating pay-for-delete (which takes months), requesting goodwill deletion (rarely successful), or waiting for the seven-year automatic removal.

Can bankruptcy remove charge-offs from my credit report?

Bankruptcy discharges your legal obligation to pay the debt, but the charge-off remains on your credit report for seven years. The account status updates to show it was included in bankruptcy.

Should I dispute a charge-off even if it’s accurate?

No. Disputing accurate information is ineffective and can be considered frivolous. Focus instead on negotiating pay-for-delete or building positive credit while waiting for automatic removal.

How do I know if a credit repair company is legitimate?

Legitimate companies provide written contracts, don’t charge upfront fees, don’t guarantee specific results, explain your legal rights, and give you time to cancel (three-day cooling-off period under CROA)[3].

Can charge-offs be removed if the creditor goes out of business?

Not automatically. If the creditor no longer exists, the charge-off may become harder to verify during disputes, potentially increasing removal chances. However, debt is often sold or transferred to other companies before a creditor closes.

Conclusion

Credit repair companies can legally dispute charge-offs and negotiate with creditors on your behalf, but they cannot remove accurate, legitimate charge-offs from your credit report. The most realistic paths to removal involve disputing genuine reporting errors, negotiating pay-for-delete agreements, or requesting goodwill deletions—all strategies you can pursue yourself for free.

Before hiring a credit repair company, carefully review your credit reports to identify specific inaccuracies. If your charge-offs are accurate, understand that no company can legally guarantee removal regardless of their marketing claims. The Federal Trade Commission’s warning is clear: no one can legally remove accurate and current negative information[6].

Your action steps:

- Obtain your credit reports from all three bureaus at AnnualCreditReport.com

- Review charge-offs carefully for errors in amounts, dates, creditor names, or account numbers

- Dispute inaccuracies directly with credit bureaus using certified mail and detailed documentation

- Negotiate pay-for-delete by contacting creditors with settlement offers and requesting written deletion agreements

- Consider professional help only if you have multiple complex disputes and lack time for the administrative work

- Build positive credit with on-time payments, low credit utilization, and new positive accounts

- Avoid scams by rejecting companies that guarantee results, charge upfront fees, or promise rapid removal

Remember that charge-offs automatically disappear after seven years from the original delinquency date[1][2]. While that may seem like a long time, focusing on building positive credit during this period often proves more valuable than spending hundreds of dollars on credit repair services that cannot legally deliver guaranteed results.

If you choose to hire a credit repair company, verify they’re compliant with CROA, check reviews with the Better Business Bureau, get everything in writing, and never pay upfront fees. But for many consumers, the DIY approach using the same legal tools available to credit repair companies offers the best combination of cost-effectiveness and realistic expectations.

References

[1] Can Credit Repair Companies Remove Charge Offs – https://www.thecreditpeople.com/credit-repair/can-credit-repair-companies-remove-charge-offs

[2] Remove A Charge Off – https://www.incharge.org/debt-relief/debt-management/remove-a-charge-off/

[3] Credit Report Charge Off Removal Services – https://www.badcredit.org/how-to/credit-report-charge-off-removal-services/

[4] Best Credit Repair Companies – https://money.com/best-credit-repair-companies/

[6] Fixing Your Credit Faqs – https://consumer.ftc.gov/articles/fixing-your-credit-faqs

Leave a Reply to Can Credit Repair Companies Really Fix Your Credit? 2026 – The Credit Repair Heros Cancel reply