Last updated: February 26, 2026

Sarah stared at her credit report in disbelief. A $340 medical collection from three years ago was blocking her mortgage approval. She’d already paid the bill, but there it sat, dragging down her score. When a credit repair company promised they could “definitely remove it,” she wondered: was this legitimate help or just another scam?

The question of can credit repair companies remove collections depends entirely on whether those collections contain errors or can’t be verified. Credit repair firms cannot legally force removal of accurate, verifiable collection accounts, but they can successfully challenge inaccurate entries or negotiate voluntary deletions with creditors.[7]

Key Takeaways

- Credit repair companies cannot legally remove accurate, verifiable collection accounts from your credit report

- Collections with errors, unverifiable information, or missing documentation can be removed with success rates exceeding 90%[1]

- Accurate collections rarely delete without leverage, with removal rates under 20%[1]

- The Fair Credit Reporting Act requires credit bureaus to investigate disputes within 30 days[1]

- Pay-for-delete agreements depend entirely on creditor discretion and require written confirmation[2]

- Collections automatically fall off credit reports seven years from the original delinquency date[1]

- DIY dispute methods follow the same legal process as credit repair companies

- Time-barred debts near the seven-year mark have higher removal chances due to missing verification documents

Quick Answer

Credit repair companies can remove collections, but only under specific conditions. If a collection account contains inaccuracies (wrong amount, incorrect dates, unverifiable ownership), credit repair firms can dispute it and often succeed in getting it deleted. However, accurate collections that creditors can verify cannot be legally forced off your report. Success depends on finding errors, negotiating pay-for-delete agreements, or waiting for the seven-year reporting period to expire.

How Do Credit Repair Companies Actually Remove Collections?

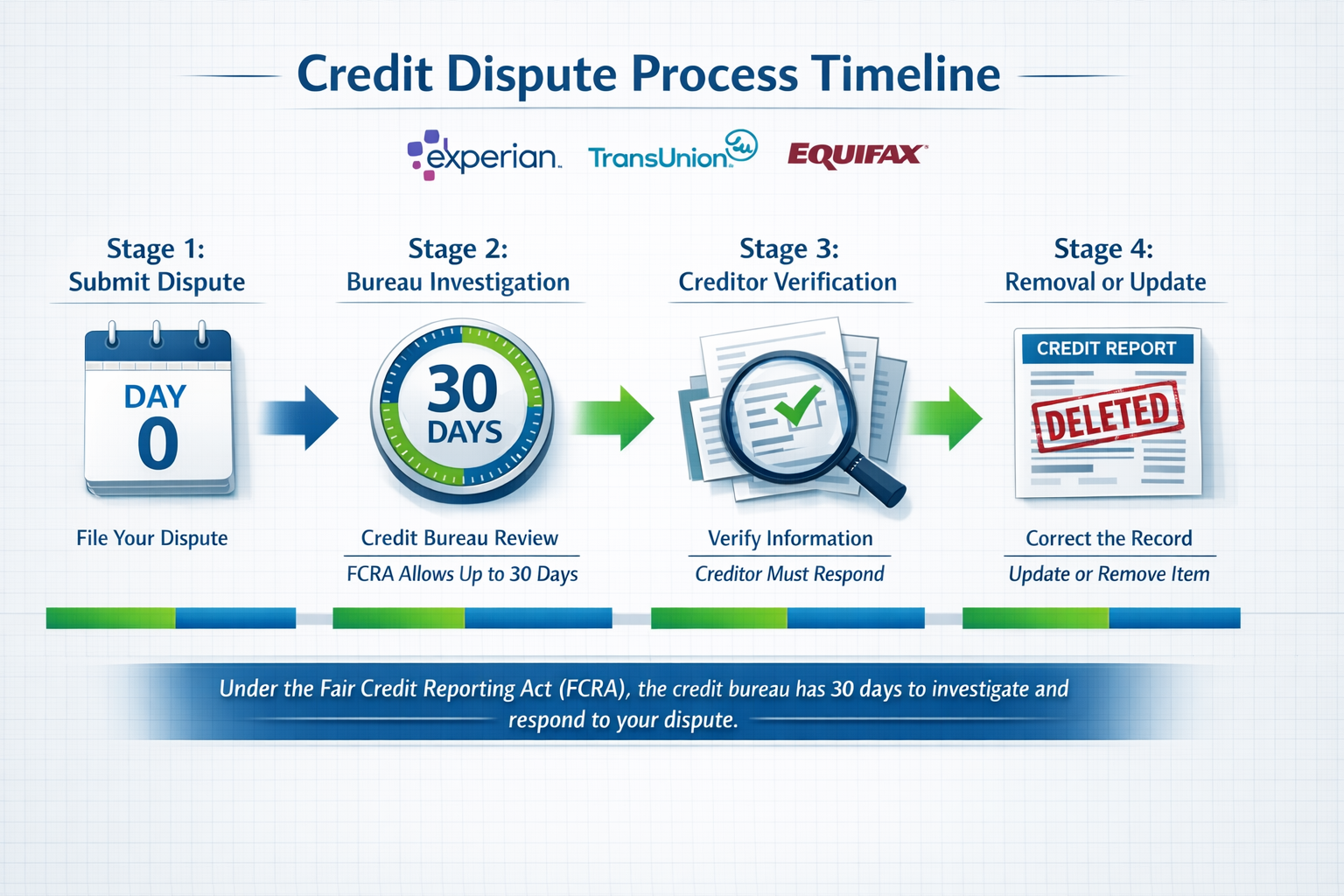

Credit repair companies remove collections by identifying weaknesses in how the debt is reported and documented, then challenging those entries through formal disputes. They cannot use secret loopholes or special connections—they follow the same legal process available to anyone under the Fair Credit Reporting Act (FCRA).[1]

The removal process works through three main strategies:

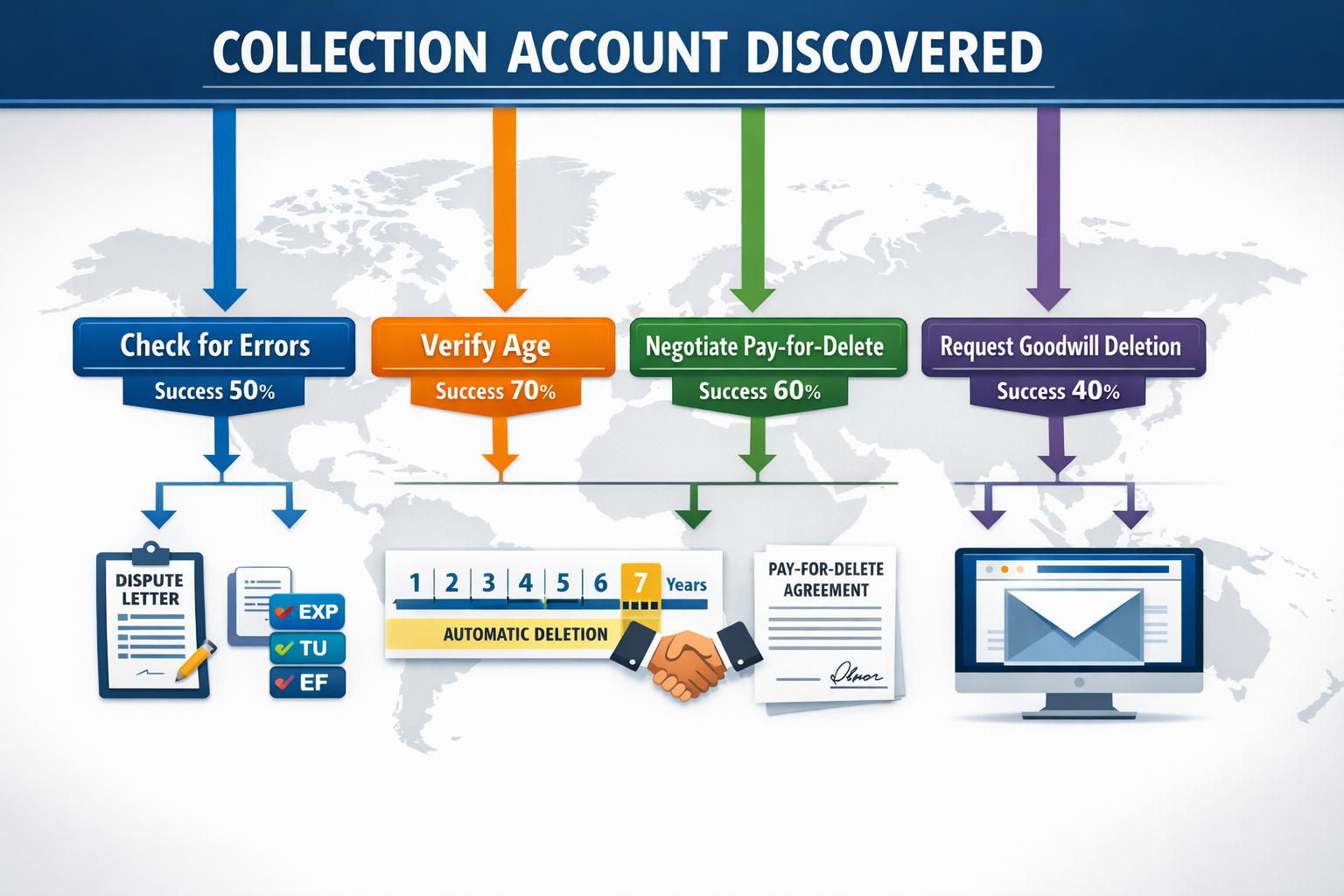

Disputing inaccuracies: Credit repair firms scrutinize collection entries for errors like wrong amounts, incorrect dates, mismatched account numbers, or ownership disputes. When they find discrepancies, they file formal disputes with credit bureaus, which must investigate within 30 days.[1]

Exploiting verification failures: Under FCRA rules, collection agencies must verify the debt’s validity when challenged. If they cannot provide adequate documentation within the investigation window (which can extend to 45 days with additional documents), the bureau must remove the entry—even if the debt is actually valid.[1]

Negotiating voluntary deletions: Credit repair companies contact creditors and collection agencies to negotiate pay-for-delete agreements or goodwill deletions. These arrangements are voluntary; creditors aren’t legally required to accept them.[1]

A documented case from January 2026 shows how this works in practice. Maurice used credit repair strategies to remove four collections and charge-offs within two dispute rounds, with his TransUnion score jumping 59 points.[3] The key was identifying data inconsistencies tied to old addresses and name variations that weakened the connection between him and the accounts.

Common mistake: Many people assume credit repair companies have special authority to delete accurate information. They don’t. The Federal Trade Commission explicitly states: “No one promising to repair your credit can legally remove information if it’s both accurate and current.”[7]

Can Credit Repair Companies Remove Accurate Collections?

Credit repair companies cannot legally force removal of accurate collection accounts that creditors can verify. The FCRA requires credit bureaus to maintain valid information for up to seven years from the original delinquency date, and no company can override this federal law.[1][7]

However, “accurate” doesn’t always mean “permanent.” Here’s what can still happen:

Pay-for-delete negotiations: Some creditors voluntarily agree to remove collection entries after receiving payment, even though the debt is accurate. Success depends entirely on the creditor’s internal policies—there’s no legal requirement for them to delete.[1] Written agreements are essential because verbal promises provide no legal protection.[2]

Goodwill deletions: For paid collections, credit repair companies may send goodwill letters requesting removal as a courtesy. This works best when you have a documented hardship (medical emergency, job loss) and a history of otherwise responsible credit use.

Aging out naturally: Collections automatically delete seven years from the original delinquency date. Credit repair companies can’t speed this up, but they can ensure bureaus comply with the timeline.[1]

Industry estimates suggest accurate collection entries have under 20% removal rates through credit repair efforts.[1] The odds improve significantly if:

- The debt is close to the seven-year mark (creditors often lack documentation for old debts)

- You can demonstrate the collection resulted from identity theft or fraud

- The original creditor has gone out of business or sold the debt multiple times

- You have leverage (like offering full payment in exchange for deletion)

Choose this approach if: You’ve verified the collection is accurate but want to explore every legal option before accepting it will remain on your report for the full seven years.

What’s the Success Rate for Removing Inaccurate Collections?

When collections contain errors or unverifiable information, success rates for complete removal exceed 90%.[1] This high success rate reflects how the FCRA investigation process works—if creditors can’t prove the debt’s validity within 30 days, bureaus must delete it.

Common inaccuracies that lead to successful removals include:

- Wrong account balances: The collection shows $500 but you only owed $350

- Incorrect dates: The delinquency date is wrong, affecting the seven-year reporting period

- Duplicate entries: The same debt appears multiple times from different collectors

- Identity errors: Wrong name spelling, address, or Social Security number digits

- Ownership disputes: The collection agency can’t prove they legally own the debt

- Statute of limitations violations: Reporting debt beyond the seven-year limit

The verification process creates natural removal opportunities. Collection agencies often purchase debt portfolios with incomplete documentation. When challenged, they may lack:

- Original creditor agreements

- Payment history records

- Proof of debt ownership transfer

- Your signature on any agreement

- Verification of the exact amount owed

Real-world example: Collections tied to old data, previous addresses, or name variations create removal opportunities by weakening the connection between you and the account.[3] If you moved several times or changed your name, the collection agency may struggle to verify the debt belongs to you specifically.

Edge case: Sometimes collections are technically accurate but reported incorrectly. For instance, the debt is valid but the creditor lists the wrong account type (medical vs. credit card) or reports it to only two bureaus instead of three. These reporting inconsistencies give you grounds for dispute.

The 30-day investigation window (up to 45 days with additional documents) typically requires 1-3 dispute rounds, stretching the total process to 2-6 months.[1] Credit repair companies often file multiple rounds because creditors sometimes provide minimal verification the first time, then fail to respond to subsequent challenges.

How Long Does the Collection Removal Process Take?

The FCRA requires credit bureaus to complete investigations within 30 days of receiving a dispute, with extensions up to 45 days if you submit additional documentation during the investigation.[1] However, the complete removal process typically takes 2-6 months because credit repair companies run multiple dispute rounds.[1]

Here’s the realistic timeline:

| Phase | Duration | What Happens |

|---|---|---|

| Initial dispute submission | Week 1 | Credit repair company files disputes with all three bureaus |

| Bureau investigation | 30-45 days | Bureaus contact creditors for verification |

| First results | Day 30-45 | Bureaus report findings (deleted, verified, or updated) |

| Second dispute round (if needed) | 30-45 days | Challenge verification quality or new inaccuracies |

| Third dispute round (if needed) | 30-45 days | Final challenges or escalation to CFPB complaint |

| Pay-for-delete negotiation | 2-8 weeks | Parallel process with creditors while disputes proceed |

Why multiple rounds matter: Creditors often provide minimal verification in the first round—just confirming the debt exists. A second dispute can challenge the quality of that verification, asking for specific documentation like original agreements or payment histories. If the creditor can’t provide detailed proof, the bureau must delete the entry.

Faster results occur when:

- The collection is clearly inaccurate (wrong person, paid debt still showing)

- The collection agency doesn’t respond within 30 days

- The debt is near the seven-year reporting limit and documentation is missing

- You provide strong evidence (receipts, validation denial letters) upfront

Slower timelines happen when:

- The creditor has complete documentation and responds promptly

- Multiple collection accounts need individual disputes

- You’re negotiating pay-for-delete (creditors may take weeks to respond)

- Bureaus request additional information, triggering the 45-day extension

Common mistake: Expecting instant results. Even when collections are obviously wrong, the legal investigation process takes time. Companies promising “24-hour deletion” are either scamming you or using illegal tactics that could backfire.

Pro tip: Time-barred debts near the seven-year reporting limit have the highest removal success rates because bureaus automatically purge valid entries upon dispute when aged debts lack adequate proof.[1] If your collection is six years old, waiting a few more months might be more effective than aggressive disputing.

What Evidence Do You Need to Remove Collections?

To successfully remove collections, you need proof that challenges the debt’s validity, accuracy, or legal reportability. The stronger your evidence, the higher your chances of deletion—credit bureaus and creditors must respond to documented proof, not just your word.[1][2]

Essential documentation includes:

For inaccurate collections:

- Credit reports from all three bureaus showing the disputed entry

- Receipts or bank statements proving you paid the debt

- Correspondence showing different amounts than what’s reported

- Identity theft reports if the debt isn’t yours

- Documentation of name changes, address changes, or data mismatches

For verification challenges:

- Debt validation letters you sent to collectors

- Responses (or lack thereof) from collection agencies

- Proof the collector didn’t respond within the required timeframe

- Evidence of ownership disputes (debt sold multiple times)

For pay-for-delete negotiations:

- Written pay-for-delete agreements before making payment[2]

- Proof of payment (never pay without a written agreement first)

- Follow-up correspondence confirming deletion terms

- Documentation of any verbal promises (though these lack legal weight)

For time-barred debts:

- Original delinquency date documentation

- Calculation showing the debt exceeds seven years

- State statute of limitations information (for legal action, not reporting)

Real scenario: When disputing a medical collection, you’d want the original hospital bill, insurance explanation of benefits, payment receipts, and correspondence with the collection agency. If the amounts don’t match or the collection agency can’t provide the original creditor agreement, you have grounds for removal.

What makes evidence compelling:

- Official documents (not just your handwritten notes)

- Dated correspondence showing timelines

- Inconsistencies between what different parties claim

- Proof of procedural violations (like failing to send required notices)

Choose this approach if: You have documentation that contradicts what’s on your credit report. Without evidence, disputes become “he said, she said” situations where bureaus typically side with creditors.

Edge case: Sometimes the best evidence is the absence of evidence. If you request debt validation and the collector never responds, that non-response becomes your proof. Save all certified mail receipts and track response deadlines carefully.

Should You Hire a Credit Repair Company or DIY?

You can legally do everything a credit repair company does yourself—the FCRA gives individuals the same dispute rights as any company. The decision to hire help or go DIY depends on your time, confidence navigating credit laws, and the complexity of your situation.

Choose DIY if:

- You have 1-2 collection accounts to dispute

- The errors are obvious (wrong amount, already paid, not your debt)

- You’re comfortable writing formal dispute letters

- You can track multiple 30-day deadlines and follow up consistently

- You want to save the $50-150 monthly fees credit repair companies charge[4]

Choose professional help if:

- You have multiple collections across different creditors

- You’re unsure what qualifies as a valid dispute reason

- You’ve tried DIY disputes without success

- You’re preparing for a major purchase (mortgage, car loan) and need faster results

- You want expert negotiation for pay-for-delete agreements

- The time investment of managing disputes yourself isn’t practical

What credit repair companies provide:

- Knowledge of which dispute reasons work best

- Template letters and documentation strategies

- Systematic tracking of all three bureaus and multiple creditors

- Negotiation experience with collection agencies

- Understanding of FCRA technicalities and creditor response patterns

What they cannot do:

- Remove accurate, verifiable information legally[7]

- Guarantee specific results or timelines

- Create new credit identities or use illegal tactics

- Improve your credit faster than you could yourself with the same strategies

Cost comparison: DIY costs only postage and certified mail fees (roughly $10-30 total). Credit repair companies charge $50-150 monthly, with most cases taking 3-6 months ($150-900 total).[4] You’re paying for expertise and time savings, not access to special powers.

Common mistake: Hiring companies that promise guaranteed deletion of accurate debts or specific score increases. Legitimate firms explain what’s possible under FCRA rules and set realistic expectations.

Middle ground option: Use credit repair software or one-time consultation services that teach you the process but let you execute it yourself. This combines expert knowledge with DIY cost savings.

What Happens After Collections Are Removed?

When collections are successfully removed from your credit report, the impact on your credit score is typically immediate but varies based on your overall credit profile. The deletion doesn’t erase the original debt’s legal status—you may still owe the money even if it’s no longer reported.

Immediate effects:

- Score increase: Most people see 20-100 point improvements, depending on how many collections are removed and what other credit factors exist

- Report updates: Changes appear within 30 days of bureau confirmation, sometimes within days for online disputes

- Improved credit mix: Removing negative items improves your payment history percentage (35% of FICO scores)

What removal doesn’t change:

- The legal obligation to pay the debt (unless you negotiated settlement or discharge)

- Other negative items still on your report

- Your actual creditworthiness for future borrowing

- The original creditor’s internal records

Important distinction: Removal from your credit report differs from debt forgiveness. If you disputed an accurate collection and won because the creditor couldn’t verify it, you may still legally owe the debt. Creditors can still sue for payment within your state’s statute of limitations (typically 3-6 years for most debts, varying by state).

Best practices after removal:

- Download updated reports from all three bureaus to confirm deletion

- Keep documentation of the removal in case it reappears (errors sometimes resurface)

- Monitor your credit monthly to catch any re-insertion attempts

- Address the underlying issue that led to collections (budget problems, medical debt, etc.)

- Build positive credit to replace the negative history with good payment patterns

Real-world scenario: After removing a $500 utility collection, your score jumps 45 points, helping you qualify for a car loan. However, the utility company still has the right to pursue the $500 debt through collections or legal action unless you’ve paid it or reached a settlement.

Edge case: Sometimes creditors re-insert deleted collections after several months, claiming they’ve now obtained proper verification. If this happens, you can dispute again and file a complaint with the Consumer Financial Protection Bureau for violating FCRA re-insertion rules.

Choose this approach if: You want to maximize the credit score benefit while understanding your legal obligations remain separate from credit reporting.

What Are the Risks of Using Credit Repair Companies?

While legitimate credit repair companies provide legal services, the industry includes scams and questionable practices that can waste your money or damage your credit further. Understanding the risks helps you avoid predatory companies and make informed decisions.

Common risks and red flags:

Financial risks:

- Upfront fees: Federal law prohibits charging before services are performed, but some companies find workarounds[7]

- Monthly charges without results: Paying $100/month for six months with no deletions

- Unnecessary services: Disputing accurate information you could simply wait to age off

- Hidden costs: Setup fees, monthly monitoring charges, or cancellation penalties

Legal and credit risks:

- Illegal tactics: Some companies advise creating new credit identities (illegal) or filing false disputes

- Worsened credit: Frivolous disputes can trigger creditor responses that add negative information

- Legal liability: If a company uses illegal methods, you could face consequences

- Debt collector attention: Disputes sometimes prompt dormant collectors to restart collection efforts

Scam warning signs:

- Guaranteeing specific score increases or deletion of accurate information

- Pressuring you to sign immediately without reviewing contracts

- Advising you not to contact credit bureaus directly

- Suggesting you dispute everything regardless of accuracy

- Requiring payment before providing any services

- Promising to create a “new credit identity” using CPNs (Credit Privacy Numbers)

Legitimate company characteristics:

- Explains your legal rights under FCRA before selling services

- Provides written contracts detailing services and costs

- Charges only after performing work

- Sets realistic expectations about outcomes

- Encourages you to check their reputation with state attorneys general

- Offers money-back guarantees if they don’t deliver results

Real example: The FTC regularly shuts down credit repair scams that charge thousands of dollars upfront, then disappear or provide no actual service. In 2025-2026, enforcement actions targeted companies making false promises about removing accurate bankruptcies and foreclosures.

Risk mitigation strategies:

- Research companies through Better Business Bureau and state consumer protection offices

- Read contracts completely before signing

- Verify the company is bonded and registered in your state (if required)

- Start with a single month to evaluate results before committing long-term

- Keep copies of all communications and documentation

Choose DIY if: You’re uncomfortable with the risk-to-benefit ratio of hiring help, especially if your collections are recent and clearly accurate.

How Do Pay-for-Delete Agreements Work?

Pay-for-delete agreements are arrangements where collection agencies or creditors agree to remove negative entries from your credit report in exchange for payment. These deals are entirely voluntary—creditors have no legal obligation to delete accurate information after receiving payment.[1]

The basic process:

- Contact the creditor or collector (not the credit bureau) to propose pay-for-delete

- Negotiate terms including the exact payment amount and deletion confirmation

- Get written agreement before sending any money[2]

- Make payment according to the agreed terms

- Verify deletion on all three credit reports within 30-45 days

- Follow up if deletion doesn’t occur as agreed

What to include in written agreements:

- Specific account number and creditor name

- Exact payment amount and payment method

- Explicit statement that the creditor will request deletion from all three bureaus

- Timeline for deletion (typically 30 days after payment)

- Confirmation that payment settles the account in full

- Signatures from both parties

Success factors:

- Timing: Creditors are most willing to negotiate when debts are old or they’ve purchased the debt for pennies on the dollar

- Leverage: Offering full payment (not settlement) increases acceptance odds

- Creditor policies: Some companies have blanket policies against pay-for-delete; others routinely accept

- Negotiation approach: Professional, written requests work better than aggressive demands

Common mistake: Paying first, then asking for deletion. Once creditors have your money, they have zero incentive to delete. Always get written confirmation before payment.[2]

Alternative approach—goodwill deletion: For debts you’ve already paid, send goodwill letters explaining the circumstances that led to the collection (medical emergency, job loss, etc.) and requesting deletion as a courtesy. This works best when:

- You have an otherwise clean credit history

- The collection was a one-time hardship situation

- You’ve been a customer of the original creditor for years

- You can demonstrate the collection is preventing a significant life goal (buying a home, etc.)

Legal reality: The credit reporting agencies’ own guidelines suggest creditors should report accurate information, making pay-for-delete ethically questionable in their view. However, it’s not illegal, and many creditors participate because it helps them collect on debts they might otherwise never recover.

Edge case: Some creditors will agree to update the status to “paid” or “settled” but refuse deletion. While not as beneficial as removal, changing the status to paid still improves your credit profile.

Frequently Asked Questions

Can credit repair companies remove collections that are accurate? No, credit repair companies cannot legally force removal of accurate, verifiable collections. However, they can negotiate voluntary pay-for-delete agreements or identify technical reporting errors even in otherwise accurate accounts.[1][7]

How much does it cost to have collections removed? DIY removal costs only postage ($10-30 total). Credit repair companies charge $50-150 monthly, with most cases taking 3-6 months ($150-900 total). Pay-for-delete agreements cost whatever payment amount you negotiate with the creditor.[4]

Will paying off collections remove them from my credit report? No, paying a collection doesn’t automatically remove it. The account updates to “paid collection” status but remains on your report for seven years from the original delinquency date unless you negotiate pay-for-delete before paying.[1]

How long do collections stay on your credit report? Collections remain on credit reports for seven years from the original delinquency date (the date you first became late with the original creditor, not when it went to collections). This timeline cannot be legally extended.[1]

Can I dispute a collection that’s mine but has wrong information? Yes, you can and should dispute any inaccurate information, even if the underlying debt is yours. Wrong amounts, dates, or account details violate FCRA accuracy requirements and provide grounds for removal.[1]

What happens if a collection agency can’t verify the debt? If the collection agency cannot provide adequate verification within 30 days of a dispute, the credit bureau must remove the collection from your report, even if the debt is actually valid.[1]

Do credit repair companies have special access to remove collections? No, credit repair companies use the same FCRA dispute process available to anyone. They have no special authority or connections—their value comes from expertise and systematic execution, not secret access.[7]

Can collections be removed before seven years? Yes, through successful disputes of inaccuracies, verification failures, pay-for-delete negotiations, or goodwill deletions. However, accurate collections that creditors can verify typically remain the full seven years unless voluntarily removed.[1]

Should I pay a collection that’s about to fall off my credit report? Generally no, unless the creditor might sue you. If a collection is 6+ years old and approaching automatic deletion, payment updates it to “paid” status, which can actually refresh it and keep it visible longer. Consult a consumer attorney for your specific situation.

Can credit repair companies guarantee results? No legitimate company can guarantee specific results because removal depends on factors outside their control (creditor verification, debt accuracy, bureau decisions). Companies promising guaranteed deletions of accurate information are using illegal tactics or scamming you.[7]

What’s the difference between credit repair and debt settlement? Credit repair focuses on removing inaccurate or unverifiable items from credit reports. Debt settlement negotiates reduced payment amounts to resolve debts, which may still show as “settled for less than owed” on your credit report.

Can I remove collections myself without hiring a company? Yes, you have the same legal rights as any credit repair company under the FCRA. You can file disputes, request debt validation, and negotiate pay-for-delete agreements yourself, saving the monthly fees companies charge.[1]

Conclusion

The answer to “can credit repair companies remove collections” is nuanced: they can remove inaccurate or unverifiable collections with high success rates (over 90%), but they cannot legally force deletion of accurate, verifiable accounts.[1] Their effectiveness depends entirely on finding errors, exploiting verification failures, or negotiating voluntary deletions with creditors.

Credit repair companies offer legitimate services for people dealing with multiple collections, complex credit situations, or those who lack time to manage the dispute process themselves. However, they follow the same legal procedures available to anyone under the Fair Credit Reporting Act—there are no secret loopholes or special connections.

Your next steps:

- Pull your credit reports from all three bureaus (free at AnnualCreditReport.com) and identify all collection accounts

- Document inaccuracies like wrong amounts, dates, or accounts that aren’t yours

- Decide DIY vs. professional help based on your situation’s complexity and your available time

- Start with verification requests to collection agencies, requiring them to prove the debt’s validity

- Dispute clear errors with credit bureaus using specific facts and supporting documentation

- Negotiate pay-for-delete for accurate collections you’re willing to pay, getting written agreements first[2]

- Monitor results and file follow-up disputes if initial attempts don’t succeed

- Build positive credit while addressing collections, since new good payment history strengthens your overall profile

Remember that legitimate credit repair—whether DIY or professional—takes time. The FCRA’s 30-day investigation window means results typically appear over 2-6 months, not overnight. Be skeptical of any company promising instant deletion of accurate information or guaranteed score increases.

Whether you choose to hire help or handle disputes yourself, understanding your rights under federal credit laws empowers you to make informed decisions and avoid scams. Collections can be removed, but success requires either genuine inaccuracies or creditor cooperation—not magic or illegal tactics.

References

[1] Can Credit Repair Companies Really Remove Collections – https://www.thecreditpeople.com/credit-repair/can-credit-repair-companies-really-remove-collections

[2] How To Legally Remove Collections From Your Credit Report After Paying Off Debt – https://rapalegal.com/resources/blog/how-to-legally-remove-collections-from-your-credit-report-after-paying-off-debt/

[3] Watch – https://www.youtube.com/watch?v=3wyS_oDGGTE

[4] Best Credit Repair Companies – https://money.com/best-credit-repair-companies/

[7] Fixing Your Credit Faqs – https://consumer.ftc.gov/articles/fixing-your-credit-faqs