Last updated: February 27, 2026

Thousands of Americans struggling with poor credit scores wonder if hiring a professional service can turn their financial situation around. Can credit repair companies really fix your credit? Yes, but only if your credit report contains inaccurate, outdated, or unverifiable information that can be legally disputed and removed. These companies cannot erase legitimate negative marks, no matter what their marketing promises suggest.

The credit repair industry has grown to a $5.98 billion market in 2026, with over 25,000 businesses competing for customers[3][4]. This explosive growth doesn’t necessarily mean these services work miracles—it reflects increased consumer demand and aggressive marketing rather than guaranteed results. Understanding what credit repair companies can and cannot do will help you decide whether paying for professional help makes sense for your situation.

Key Takeaways

- Credit repair companies can only dispute and potentially remove inaccurate or unverifiable information from your credit reports, not legitimate negative marks

- The average consumer saw just a 14-point FICO score increase from 2018 to 2023, despite the industry’s revenue growth[6]

- Monthly fees typically range from $79 to $139.99, with setup fees between $19 and $195[1]

- You can legally perform all credit repair actions yourself for free under the Fair Credit Reporting Act (FCRA)

- Disputing genuine errors is one of the most effective credit repair strategies and can lead to fast score improvements[8]

- The process takes time—expect 30 to 45 days per dispute round, with no guarantees of success

- Reputable companies offer 90-day money-back guarantees and transparent pricing[1]

Quick Answer

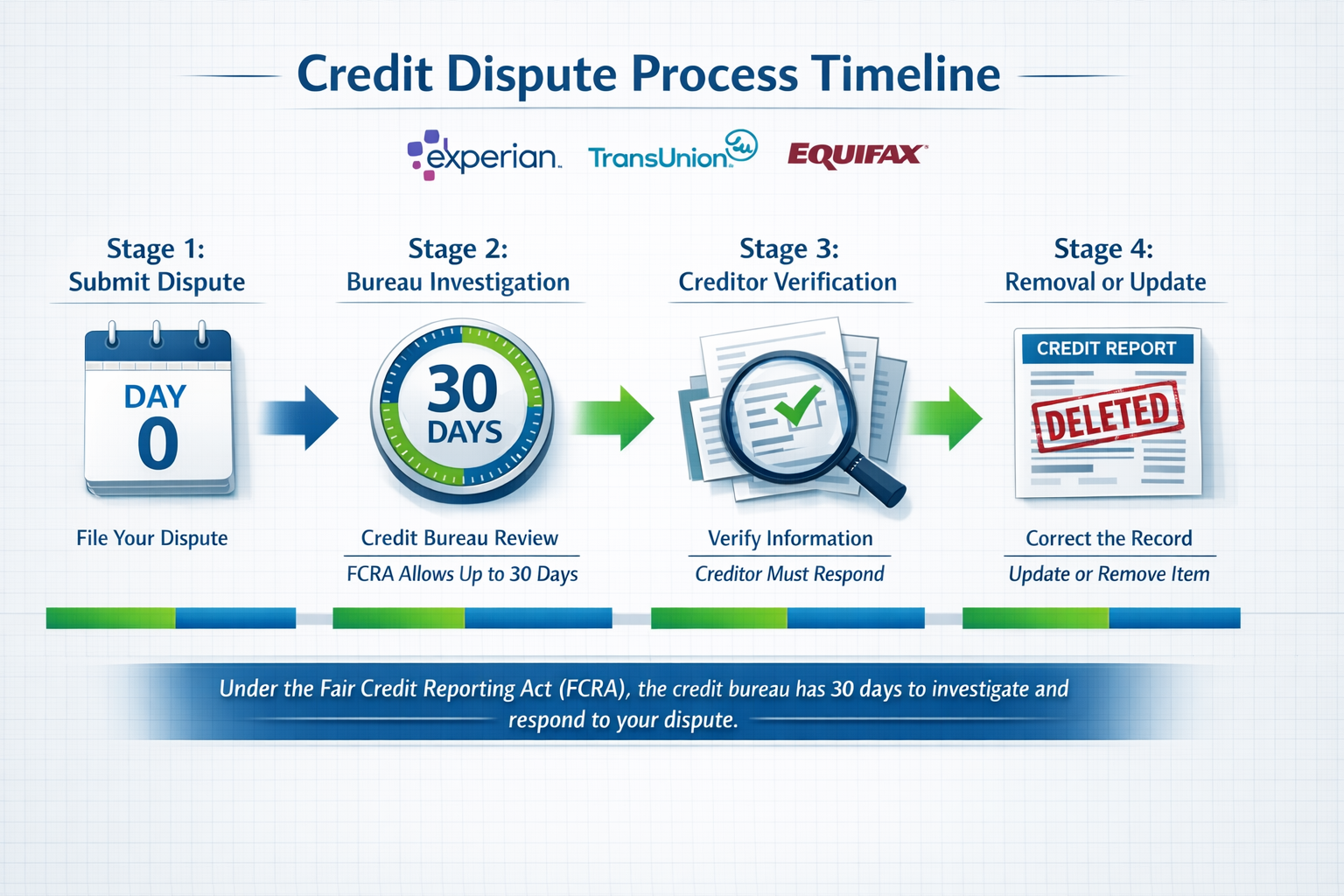

Credit repair companies can fix your credit if it contains errors, but they can’t remove accurate negative information. They work by identifying inaccuracies on your credit reports and disputing them with the three major credit bureaus (Equifax, Experian, and TransUnion). If the bureaus can’t verify the disputed items within 30 days, those items must be removed. However, anything you pay a company to do, you can legally do yourself for free.

What Do Credit Repair Companies Actually Do?

Credit repair companies identify and dispute potentially inaccurate, outdated, or unverifiable negative items on your credit reports. They act as intermediaries between you and the credit bureaus, handling the paperwork and follow-up required for formal disputes.

Here’s what the process typically involves:

Initial Credit Analysis

- Pull reports from all three major bureaus

- Review for errors, duplicates, or outdated information

- Identify items that might be disputed successfully

- Create a customized action plan

Dispute Filing and Management

- Draft formal dispute letters to credit bureaus

- Submit disputes for questionable items

- Track responses and investigation timelines

- File additional rounds of disputes if needed

Creditor Communication

- Contact original creditors for verification

- Request debt validation when appropriate

- Negotiate with collection agencies in some cases

Ongoing Monitoring

- Track changes to your credit reports

- Alert you to new negative items

- Provide monthly progress updates

Modern credit repair services increasingly use AI-powered tools for credit score analysis and dispute automation[3]. This technology helps identify patterns and potential errors more efficiently than manual review, though it doesn’t change the fundamental legal limitations of what can be removed.

What they cannot legally do:

- Remove accurate negative information

- Create a new credit identity for you

- Guarantee specific score increases

- Charge upfront fees before performing services (illegal under federal law)

Can Credit Repair Companies Really Fix Your Credit If Errors Exist?

Yes, credit repair companies can effectively fix your credit when legitimate errors exist on your reports. Disputing inaccuracies is identified as one of the most effective credit repair moves, with corrections potentially leading to fast score improvements[8].

The Fair Credit Reporting Act (FCRA) requires credit bureaus to investigate disputes within 30 days and remove any information they cannot verify. This creates the legal framework that makes credit repair possible.

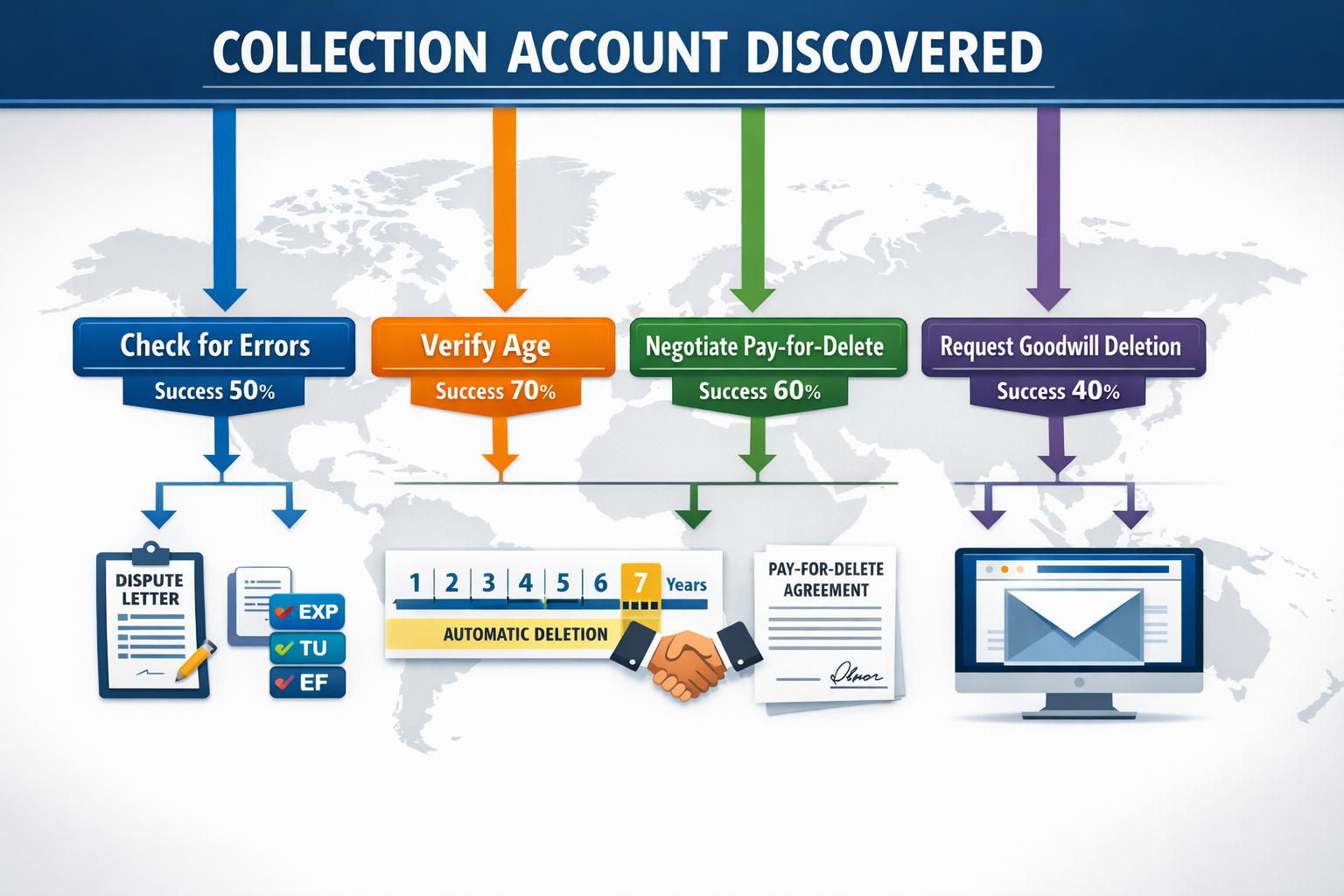

Common errors worth disputing:

- Accounts that don’t belong to you (identity theft or mixed files)

- Duplicate accounts listed multiple times

- Incorrect payment statuses or late payment dates

- Accounts reporting past the legal reporting period (typically 7 years for most negatives, 10 years for Chapter 7 bankruptcy)

- Incorrect balances or credit limits

- Closed accounts still showing as open

- Settled debts still showing balances owed

Success rates vary based on:

- Whether the error is genuinely inaccurate versus just negative

- How well the original creditor maintains records

- The age of the account (older accounts are harder to verify)

- The type of negative item being disputed

A common mistake consumers make is expecting companies to remove accurate negative information. If you legitimately missed payments or defaulted on a loan, those marks will typically remain for seven years regardless of how many times you dispute them. The bureaus will verify the information with the creditor and the negative item will stay on your report.

Choose a credit repair company if:

- You’ve identified errors but feel overwhelmed by the dispute process

- You have multiple complex errors across all three bureaus

- You lack time to manage disputes yourself

- You want professional guidance on prioritizing which items to dispute first

How Much Do Credit Repair Services Cost in 2026?

Credit repair companies charge monthly fees ranging from $79 to $139.99, with initial setup fees between $19 and $195[1]. Most reputable services offer 90-day money-back guarantees if they don’t remove at least one item from your reports.

Typical pricing structure:

| Company | Setup Fee | Monthly Fee | Money-Back Guarantee |

|---|---|---|---|

| The Credit People | $19 | $79 | 90 days |

| Sky Blue Credit | $79 | $79 | 90 days |

| CreditRepair.com | $99.95 | $99.95 | 90 days |

| Credit Saint | $195 | $79.99-$139.99 | 90 days |

Most companies operate on a month-to-month basis, meaning you can cancel anytime. However, credit repair is a time-intensive process with no immediate results possible[2][7]. Expect to pay for at least 3-6 months of service to see meaningful results, putting total costs between $237 and $839 or more.

Hidden costs to consider:

- Some companies charge per item disputed rather than flat monthly fees

- Premium tiers offer additional services like identity theft insurance

- You may need to purchase credit monitoring separately

- Opportunity cost of monthly fees versus using that money to pay down debt

Red flags for pricing scams:

- Upfront fees before any work is performed (illegal under federal law)

- Guarantees of specific score increases

- Pressure to sign long-term contracts

- Vague pricing without clear breakdowns

For comparison, doing it yourself costs nothing except your time. The FCRA gives you the same legal rights to dispute errors that credit repair companies use.

What Can’t Credit Repair Companies Remove From Your Credit?

Credit repair companies cannot legally remove accurate negative information from your credit report, regardless of their marketing claims. This fundamental limitation means they can’t help everyone who hires them.

Items that will stay if accurate:

- Late payments you actually made

- Charge-offs from legitimate unpaid debts

- Collections for debts you owe

- Bankruptcies filed within the past 7-10 years

- Foreclosures within the past 7 years

- Repossessions for vehicles you defaulted on

- Tax liens (though these no longer appear on most credit reports as of 2018)

- Hard inquiries from credit applications you authorized

The only way accurate negative information disappears is through the passage of time. Most negative marks fall off after seven years, though Chapter 7 bankruptcies remain for 10 years.

Some companies use aggressive tactics to try removing accurate information, such as:

- Filing frivolous disputes hoping creditors won’t respond in time

- Exploiting technicalities in how information is reported

- Overwhelming bureaus with repetitive disputes

These approaches rarely work long-term. Even if an item is temporarily removed, creditors can re-report accurate information, putting it back on your report.

Edge case: Sometimes accurate negative information is reported incorrectly (wrong date, wrong amount, wrong status). In these cases, you can dispute the inaccuracy even though the underlying debt is real. For example, if a late payment from March 2024 is incorrectly listed as being from March 2023, that’s a legitimate dispute.

For specific guidance on removing certain types of negative marks, see our detailed guides on whether credit repair companies can remove collections and if they can remove charge-offs.

DIY Credit Repair vs. Hiring a Professional Service

You can legally perform all credit repair actions yourself for free. The same FCRA rights that credit repair companies use are available to every consumer. The question becomes whether the convenience and expertise justify the monthly cost.

DIY credit repair advantages:

- Zero cost except your time

- Complete control over the process

- Direct communication with bureaus and creditors

- No risk of scams or disreputable companies

- Builds your understanding of credit systems

DIY credit repair disadvantages:

- Time-intensive (several hours per month)

- Requires learning dispute procedures

- Easy to make mistakes that weaken disputes

- No professional guidance on strategy

- Can feel overwhelming with multiple errors

Professional service advantages:

- Saves you time and effort

- Experience with effective dispute strategies

- Handles all correspondence and follow-up

- May identify errors you missed

- Some offer additional services (credit monitoring, identity theft protection)

Professional service disadvantages:

- Monthly costs of $79-$139.99 or more[1]

- Cannot do anything you can’t do yourself

- Industry includes many disreputable companies

- No guaranteed results

- Some use aggressive tactics that may backfire

Choose DIY if:

- You have only a few errors to dispute

- You’re comfortable writing formal letters

- You have time to manage the process

- You want to save money

- You prefer direct control

Choose professional services if:

- You have complex errors across multiple reports

- You lack time for the dispute process

- You feel overwhelmed by credit report complexity

- You want expert guidance on prioritization

- The monthly cost fits your budget

A middle-ground option is using free or low-cost online tools that guide you through DIY disputes while providing templates and tracking. Many nonprofit credit counseling agencies also offer free credit report review and dispute assistance.

How Long Does Credit Repair Actually Take?

Credit repair is fundamentally time-consuming with no immediate results possible[2][7]. Each dispute round takes 30 to 45 days for credit bureaus to investigate, and most people need multiple rounds to address all errors.

Realistic timeline expectations:

Month 1-2: Initial Analysis and First Disputes

- Pull and review all three credit reports

- Identify errors and create dispute strategy

- File first round of disputes

- Wait for bureau investigations (30 days)

Month 3-4: Review Results and Second Round

- Receive investigation results

- File follow-up disputes for items not removed

- Dispute any new errors discovered

- Wait for second investigation period

Month 5-6: Final Disputes and Monitoring

- Address remaining errors

- Monitor for re-insertion of deleted items

- Begin positive credit-building activities

- Evaluate overall progress

Most people see their first results within 60-90 days, but achieving maximum improvement often takes 6-12 months. The average consumer’s FICO score increased by only 14 points from 2018 to 2023[6], suggesting modest improvements are typical even with professional help.

Factors affecting timeline:

- Number of errors on your reports

- How quickly creditors respond to verification requests

- Whether items are re-inserted after initial removal

- Complexity of your credit situation

- How many dispute rounds are needed

Common mistake: Expecting overnight results. Companies that promise “fast credit repair” or “guaranteed score increases in 30 days” are using misleading marketing. The legal dispute process has built-in timeframes that cannot be shortened.

What speeds up the process:

- Accurate identification of genuine errors

- Well-documented disputes with supporting evidence

- Focusing on high-impact errors first

- Simultaneously building positive credit (on-time payments, low utilization)

What slows it down:

- Disputing accurate information (wastes time and rounds)

- Poorly written disputes without specifics

- Creditors who respond quickly with verification

- Multiple errors requiring sequential dispute rounds

Red Flags: How to Spot Credit Repair Scams

Consumer skepticism and fraud concerns remain significant industry challenges[2]. Knowing the warning signs helps you avoid disreputable companies that take your money without delivering results.

Major red flags:

🚩 Upfront fees before performing any work – Illegal under the Credit Repair Organizations Act (CROA)

🚩 Guarantees of specific score increases – No one can guarantee results since outcomes depend on what’s actually on your report

🚩 Promises to remove accurate negative information – Legally impossible and a sign of fraudulent practices

🚩 Advice to dispute everything – Wastes time and money; only errors should be disputed

🚩 Suggestions to create a new credit identity – Illegal and constitutes fraud

🚩 Pressure to sign immediately – Reputable companies let you review terms carefully

🚩 No written contract – CROA requires detailed written agreements

🚩 Refusal to explain your legal rights – Companies must inform you of rights under FCRA

🚩 Telling you not to contact credit bureaus directly – You have the legal right to communicate directly

🚩 No physical address or unclear company information – Makes it hard to pursue complaints

Notable industry incident: Lexington Law, one of the largest credit repair companies, was involved in a class action lawsuit with complaints that the company was not effectively repairing credit[5]. This highlights that even well-known companies face scrutiny and consumer complaints.

How to verify legitimacy:

- Check Better Business Bureau ratings and complaint history

- Read recent customer reviews on independent sites

- Verify the company has been in business for several years

- Confirm they offer a money-back guarantee

- Ensure all terms are clearly explained in writing

- Look for transparent pricing without hidden fees

Regulatory framework: The FCRA heavily shapes industry operations, with stringent regulations limiting aggressive tactics and protecting consumer rights[2]. Regulatory scrutiny intensified in 2020, and new legislation was proposed in 2023 to further regulate the industry[2].

Top Legitimate Credit Repair Companies in 2026

Leading companies include Credit Saint, Sky Blue Credit, Lexington Law, CreditRepair.com, The Credit People, and others[1][2]. These established providers offer transparent pricing, money-back guarantees, and clear explanations of services.

What makes a company reputable:

- Years of established operation (5+ years)

- Clear, transparent pricing structure

- 90-day or longer money-back guarantee

- Positive customer reviews from independent sources

- No upfront fees before service begins

- Detailed written contracts explaining services

- Responsive customer service

- Educational resources about credit

Service features to look for:

- Disputes filed with all three credit bureaus

- Monthly progress reports and updates

- Credit monitoring and score tracking

- Mobile app for easy access

- Educational resources and credit coaching

- Intervention for identity theft issues

- Goodwill letter assistance for creditors

Pricing considerations: Services range from $19 setup fees with $79 monthly charges (The Credit People, Sky Blue Credit) to $195 setup fees with $139.99 monthly charges (Credit Saint’s premium tier)[1]. Higher prices don’t always mean better results—evaluate based on services included and customer reviews.

Questions to ask before signing up:

- What specific services are included in the monthly fee?

- How long is the money-back guarantee period?

- What happens if no items are removed?

- Can I cancel anytime without penalties?

- How will you communicate progress to me?

- Do you dispute with all three bureaus?

- What additional fees might I encounter?

Technology integration has become central to operations, with leading companies utilizing AI-powered tools for credit score analysis and dispute automation[3]. This can improve efficiency but doesn’t change the fundamental legal limitations of what can be removed.

Alternatives to Credit Repair Companies

Several alternatives exist for people who want to improve their credit without paying monthly fees to a credit repair service.

Free DIY dispute process:

- Request free credit reports from AnnualCreditReport.com

- Review for errors, duplicates, and outdated information

- File disputes directly with credit bureaus online or by mail

- Follow up on investigations and results

- Repeat as needed for remaining errors

The Consumer Financial Protection Bureau (CFPB) provides free sample dispute letters and step-by-step guidance.

Nonprofit credit counseling:

- Free or low-cost services from HUD-approved agencies

- Credit report review and error identification

- Dispute assistance and guidance

- Debt management plans for those with unmanageable debt

- Financial education and budgeting help

Find legitimate counselors through the National Foundation for Credit Counseling (NFCC).

Credit monitoring services:

- Track changes to your credit reports automatically

- Alert you to new errors or potential identity theft

- Some offer dispute assistance tools

- Often cheaper than full credit repair services

- Many credit card companies offer free monitoring

Positive credit building:

- Make all payments on time (35% of FICO score)

- Pay down credit card balances (30% of FICO score)

- Become an authorized user on someone’s good account

- Open a secured credit card to establish positive history

- Keep old accounts open to maintain credit history length

Debt settlement or management:

- For those with legitimate debts they can’t pay

- Negotiate directly with creditors for reduced balances

- Work with nonprofit debt management programs

- Consider whether bankruptcy might be appropriate for severe situations

When to use each alternative:

- DIY disputes: You have a few clear errors and time to manage the process

- Credit counseling: You need guidance but can’t afford paid services

- Credit monitoring: You want ongoing protection and alerts

- Positive building: You have no errors but need to rebuild after legitimate negatives

- Debt settlement: You have real debts you cannot pay in full

For more information on specific strategies, explore resources on credit score improvement and consumer credit management.

Frequently Asked Questions

Can credit repair companies guarantee they’ll fix my credit? No legitimate company can guarantee specific results. Credit repair outcomes depend entirely on whether your reports contain inaccurate information that can be successfully disputed and removed. Companies that promise guaranteed score increases are using deceptive marketing.

How much will my credit score increase with credit repair? It varies widely based on your individual situation. The average consumer saw just a 14-point FICO score increase from 2018 to 2023[6]. If you have multiple significant errors removed, you might see larger improvements. If your negative items are accurate, you’ll see little to no improvement.

Is it worth paying for credit repair or should I do it myself? DIY credit repair costs nothing except time and gives you the same legal rights as paid services. Pay for professional help if you have complex errors across multiple reports, lack time for the process, or want expert guidance. Skip paid services if you have just a few errors and feel comfortable managing disputes yourself.

How long do negative items stay on my credit report? Most negative items remain for seven years from the date of first delinquency. Chapter 7 bankruptcies stay for 10 years. Hard inquiries remain for two years but only affect scores for one year. Positive information can stay indefinitely.

Can credit repair companies remove collections from my credit report? They can remove collections that are inaccurate, unverifiable, or past the legal reporting period. They cannot remove accurate collections within the seven-year reporting window. Learn more in our guide on removing collections.

What’s the Credit Repair Organizations Act (CROA)? CROA is federal law that regulates credit repair companies. It prohibits upfront fees before services are performed, requires written contracts, mandates disclosure of consumer rights, and bans false advertising. It gives you the right to cancel within three days of signing.

Do credit repair companies work with all three credit bureaus? Reputable companies dispute errors with all three major bureaus (Equifax, Experian, and TransUnion) because creditors don’t report to all three consistently. Your reports may differ across bureaus, so comprehensive service addresses all three.

Can I repair my credit if I’ve filed for bankruptcy? Yes, but credit repair can’t remove an accurate bankruptcy filing. It can remove errors related to accounts included in bankruptcy (like debts still showing balances after discharge) or other unrelated inaccuracies. Building positive credit after bankruptcy is often more effective than disputing the bankruptcy itself.

What happens if a disputed item is removed but then reappears? This is called “re-insertion.” If a creditor provides verification after initially failing to respond, the item can be put back on your report. The bureau must notify you within five days of re-insertion. You can dispute again with additional documentation or request the creditor’s verification evidence.

Are there credit repair services specifically for business credit? Yes, some companies specialize in business credit repair, which involves different bureaus (Dun & Bradstreet, Experian Business, Equifax Business) and different reporting rules. Business credit repair follows similar principles but requires industry-specific expertise.

How do I file a complaint against a credit repair company? File complaints with the Consumer Financial Protection Bureau (CFPB), your state attorney general’s office, and the Federal Trade Commission (FTC). You can also report to the Better Business Bureau and leave reviews warning other consumers.

Will using a credit repair company hurt my credit score? No, the dispute process itself doesn’t hurt your score. However, if you stop making payments on legitimate debts while disputing them, those new late payments will damage your credit. Continue meeting all financial obligations during the credit repair process.

Conclusion

Can credit repair companies really fix your credit? The answer depends entirely on what’s wrong with it. If your credit reports contain errors, outdated information, or unverifiable negative items, credit repair companies can successfully dispute and remove them, potentially improving your score. However, they cannot legally remove accurate negative information, no matter how much you pay or what they promise.

The credit repair industry generated $5.98 billion in revenue in 2026[3], but the average consumer saw only modest score improvements over recent years[6]. This gap between industry growth and actual results highlights an important truth: credit repair is not a magic solution, and many people would achieve the same results doing it themselves for free.

Your next steps:

- Pull your credit reports from all three bureaus at AnnualCreditReport.com

- Review carefully for errors, duplicates, and outdated information

- Decide your approach based on the complexity of errors and your available time

- If hiring help, choose a reputable company with transparent pricing and money-back guarantees

- If going DIY, use free resources from the CFPB and nonprofit credit counselors

- Focus on positive building alongside error disputes for maximum improvement

- Set realistic expectations about timelines (3-6 months minimum) and potential score increases

Remember that legitimate credit repair takes time, and there are no shortcuts to removing accurate negative information. The most effective long-term strategy combines disputing genuine errors with building positive credit through on-time payments, low credit utilization, and responsible financial management.

Whether you choose professional help or the DIY route, understanding your rights under the Fair Credit Reporting Act empowers you to make informed decisions about your credit repair journey. For more guidance on specific credit challenges, explore The Credit Repair Heros resources on topics ranging from dispute strategies to collection account removal.

References

[1] Best Credit Repair Companies – https://money.com/best-credit-repair-companies/

[2] Credit Repair 1929343 – https://www.datainsightsmarket.com/reports/credit-repair-1929343

[3] Credit Repair Services – https://www.researchandmarkets.com/report/credit-repair-services

[4] ibisworld – https://www.ibisworld.com/united-states/industry/credit-repair-services/5741/

[5] Watch – https://www.youtube.com/watch?v=sxwhLbZ7PNo

[6] Credit Repair Statistics – https://www.consumeraffairs.com/finance/credit-repair-statistics.html

[7] How To Repair Your Credit Score In Proven Strategies That Actually Work – https://www.amerisave.com/learn/how-to-repair-your-credit-score-in-proven-strategies-that-actually-work

[8] 7 Credit Repair Moves For 2026 Before You Apply For Anything – https://creditrepairchamp.com/7-credit-repair-moves-for-2026-before-you-apply-for-anything/